Goldman Sachs predicts the calm markets will continue next year and found the stocks that thrive in a low-volatility environment.

The firm recommends a strategy based on a ratio from a Nobel Prize–winning economist.

“Low volatility across asset classes has been a defining characteristic of 2017. For equities, realized volatility ranks in the 1st percentile since 1950. Implied volatility suggests this regime will persist in 2018. Our High Sharpe Ratio basket outperforms min vol strategies and the S&P 500 during low volatility environments,” Goldman’s chief U.S. equity strategist, David Kostin, wrote in a note to clients Friday. “Our rebalanced basket offers 3x the expected return of the median S&P 500 stock with similar implied 6-month volatility.”

The Sharpe ratio was developed by economist William Sharpe, a Nobel laureate, in the 1960s. It measures the average performance of a security in excess of a risk-free return, adjusted for price volatility.

Kostin said the firm’s portfolio based on the ratio has outperformed the S&P 500 by 2 percentage points year to date. The basket includes the 50 S&P 500 stocks with the “highest prospective Sharpe ratios” using Wall Street consensus forecasts and the volatility implied by stock option prices.

The strategy has beaten the market by 7 percentage points per year since 1999, according to Kostin. His year-end 2018 target for the S&P 500 is 2,850, representing 7 percent upside to Friday’s close.

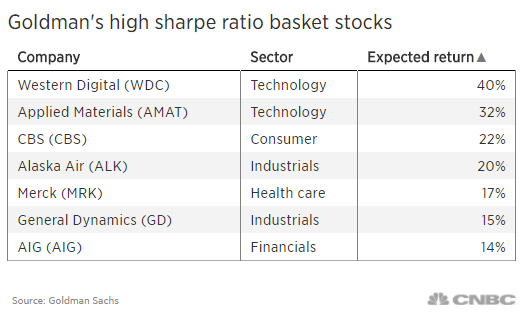

Here is a selection of seven Goldman Sachs high Sharpe ratio basket stocks.

Goldman expects another calm and rising market next year and has a strategy to capitalize on it