To some degree, Wall Street economists and strategists are tasked with telling the future. Predictions are often based on historical research and analysis, and their firms (and clients) hope they’re on the mark.

But according to Deutsche Bank’s chief international economist, Torsten Slok, forecasts for one of the economy’s benchmark measurements, the rate on the 10-year Treasury note, have been “consistently wrong” and too optimistic for the last decade and a half.

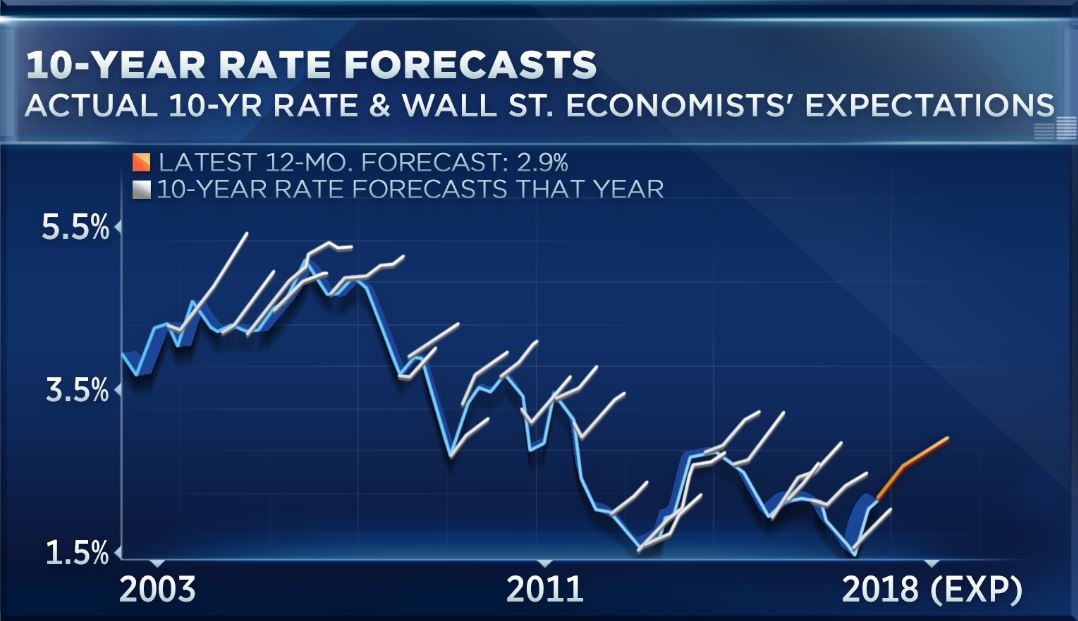

In fact, according to Slok’s measurement — analyzing the responses to the Federal Reserve’s quarterly Survey of Professional Forecasters versus the actual 10-year rate — the average 12-month forecast error since 2003 has been 60 basis points too high.

“Trends have gone down in long-term interest rates. The 10-year rate has continuously been undershooting what predictions were from the Street. So basically, Wall Street has been too optimistic on what interest rates will do,” Slok said Friday on CNBC’s “Trading Nation.”

The 10-year Treasury yield on Monday ticked down near its postelection low around 2.12 percent; the latest 12-month forecast (for the second quarter of this year) according to the Survey of Professional Forecasters, published by the Philadelphia Fed, is 2.9 percent.

Slok acknowledged that he is among the community magnified in these results. He offered one cause of misforecasting as the Street taking its cues from the Federal Reserve.

“Well, our excuse is that the Fed, in particular, for the last eight or nine years since the crisis has also been too optimistic. So maybe we’ve been taking our guidance from them. But the bottom line remains that the optimism has been there, and the whole economics profession has just not been very good at predicting what interest rates will do,” he said.

One cause of declining rates continuing to fall over the years is that the models utilized by the Fed and Wall Street have “been very focused on the U.S.,” Slok said, whereas over the last few years, stimulative monetary policies from the European Central Bank and the Bank of Japan have played a crucial role in holding interest rates down.

“The very critical thing to understand about rates — also where we stand today — is that they have been very critically driven by developments in the rest of the world. And, given that the rest of the world has had a weak recovery, they’ve had low interest rates,” he said.

Slok added: “This has been a significant flow of money, a tsunami of money has been coming from the rest of the world to the U.S., in particular U.S. fixed income, and that has been suppressing U.S. yields for quite some time now.”

The central bank last raised its federal funds target rate earlier this month, with an increase of one quarter of a point. The hike was the second announced this year. While the 10-year note yield has fallen, equities have risen to all-time highs this year, appearing to give mixed messages about the health of the economy.

“From a pure economic perspective, what we really are waiting for is inflation. The Fed has been saying for a while now that they want to raise rates. And, the Fed is clearly saying they want to raise rates a lot faster than what the market believes,” Slok said Friday.

Wall Street economists have been ‘consistently wrong’ in 10-year rate forecasts, and here’s why