A sharp drop in bullish bets on oil prices could be a contrarian signal that crude futures don’t have much further to fall and may have even finally hit bottom.

Speculative bets that U.S. crude prices will rise surged earlier this year, creating a crowded trade that was eventually undercut by higher-than-expected output growth from U.S. oil fields and a slower-than-anticipated drop in global stockpiles. Oil bears pounced, but will now have a tougher time driving down prices because bullish bets have already tumbled from record highs.

Hedge funds and other money managers have cut their long positions, or bets that crude prices will rise, to the lowest level since November, according to data from the U.S. Commodities Futures Trading Commission covering the week through June 20. At the same time, short positions, or bets that prices will fall, have risen toward record highs.

That further shrank the ratio of long to short positions, which had blown out earlier this year after money managers piled into the bull trade as OPEC began cutting its oil output in a bid to shrink global crude stockpiles and stabilize prices. The ratio now stands at roughly 2-to-one, down from a recent high of about 12-to-one in February.

The current number of short positions is unsustainable, and traders will eventually have to cover those positions, which should push up oil prices, said Tamar Essner, director of energy and utilities at Nasdaq Corporate Solutions.

“We are not yet at the highest level of short positions on record, but nearing it, which means we could start to move higher in the back half of the year,” she told CNBC.

Benchmark oil prices rose more than 2 percent on Tuesday as traders covered short positions.

To be sure, this is just one of many metrics analysts watch, Essner warned. The market is still long oil prices, and it could flip into a net short position.

While the market could yet fall further than the recent 10-month intraday low of $42.05, a drastic move below $40 a barrel likely wouldn’t last long, Essner said. She doesn’t see the market moving much lower than current levels, though sentiment will largely focus on how quickly global stockpiles fall.

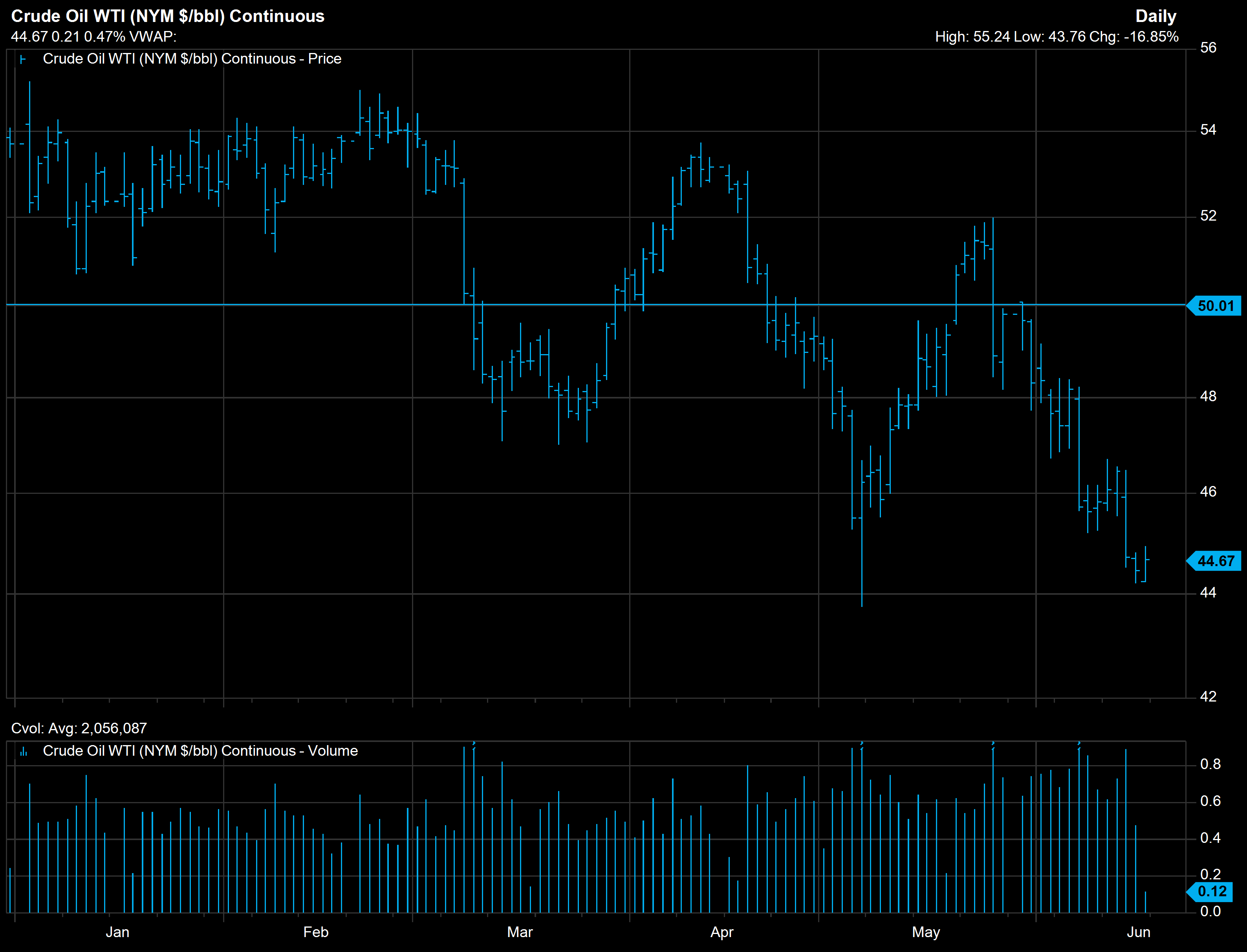

U.S. West Texas Intermediate crude futures (year to date), source: Factset

OPEC and other exporters have so far had little success driving down those levels. The producers agreed to cut roughly 1.8 million barrels a day through the first six months of this year and last month extended the agreement through March.

“The hedge fund community has clearly lost their faith in OPEC and the Saudis to be able to achieve balance, which was a much ballyhooed position over the last couple of months,” said John Kilduff, founding partner at energy hedge fund Again Capital.

But at this point, the risk of opening new short positions is beginning to outweigh the potential reward, he said.

The potential gains from shorting oil looked good when it was trading above $50, but consensus is forming around the notion that oil prices will bottom out in the upper $30 range, Kilduff said. With oil trading around $44 a barrel, potential rewards are getting slimmer, while a geopolitical shock that sends oil significantly higher would make a new short position costly.

“We’ve fallen a long way. If you’re initiating a short position now, you missed a lot of the ride down,” Kilduff said.

Source: Investment Cnbc

Oil prices may have finally hit bottom now that bullish hedge funds have thrown in the towel