Exactly a decade ago, it was time for investors to start worrying, even as stocks sat at record highs and the signs of onrushing danger were far from obvious.

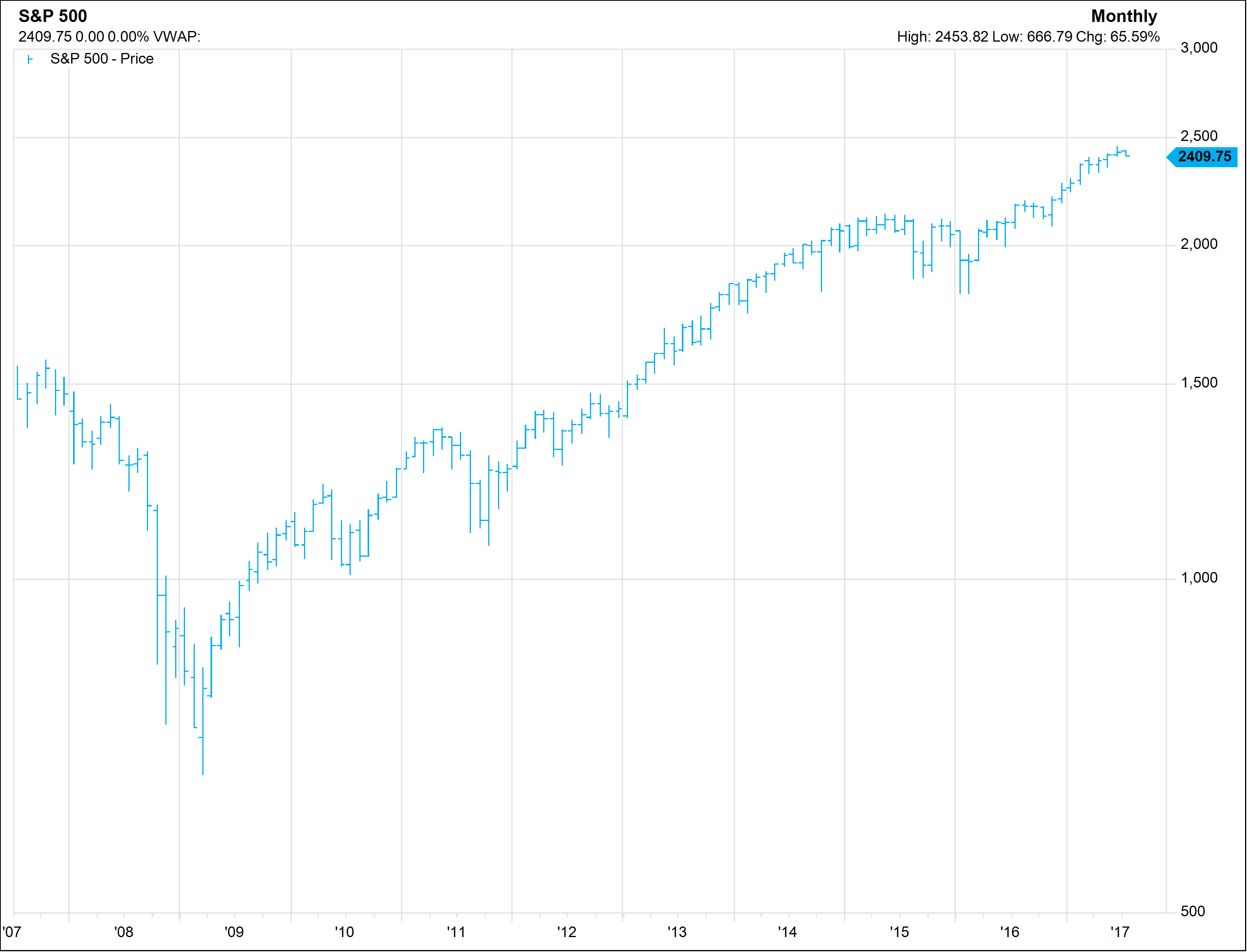

In July 2007, the U.S. stock market was just emerging from a prolonged stretch of unusual calm, the S&P 500 clicking to a new high before buckling for a 9 percent loss over the next month, as cracks emerged in the housing and credit markets.

That, as it turned out, was a warning tremor, as stocks recovered to make a slight fresh high that October, before the full force of the housing bust, Great Recession and financial crisis would wipe out half the market’s value over the next 18 months.

There’s no essential significance to the nearby tenth anniversary of the start of the last bull market’s topping process, of course. Still it presents a decent little excuse to compare current conditions with those that prevailed in the summer of 2007.

S&P 500, 10 years

Source: FactSet

The good news: While there are some parallels between July 2007 and 2017 – elevated equity valuations, a mature economic expansion, high corporate debt levels and broad expectations of improving earnings in the year to come – the crucial factors that presaged the ’07 market peak are not present.

The leading indicators of the economy, the credit backdrop and the comportment of the stock market itself are all in much better shape now than they were then. On the other hand, few saw the dangers coming on as fast as they did a decade ago, so it makes sense to be watchful for those factors turning from benign to hostile.

Here’s a side-by-side look at the setup today versus ten years ago:

Stocks appear a bit richer today, by most measures. The price-to-earnings ratio of the S&P 500, based on the past 12 months’ results, was 16.2 in July 2007, the forward P/E was 15 and the so-called Shiller P/E that uses the prior ten years’ average real earnings was 27.4. Today, the comparable figures are 20.7 trailing, 17.5 forward and Shiller P/E of 29.7.

Of course, valuation was not the trigger for the collapse in ’07. The fact that earnings began to sag and financial-company profits – the single largest segment – proved largely illusory was the critical driver.

In the one, two, five and ten years before the summer of ’07, the S&P 500 had delivered rather similar performance to the most recent comparable periods. But here again, the gains – such as the 14.6 percent trailing five-year annualized return right now – are right in line with typical bull-market tallies, and if anything the ten-year 7% annual pace is far shy of where it usually gets to at a market peak.

By mid-2007, financial stocks had begun lagging the S&P 500, and they never rebounded with the market after that 9-percent S&P summer pullback. The market was narrowing conspicuously, with small caps having lagged for more than a year.

The percentage of S&P stocks in an uptrend (above their 200-day average) peaked in February 2007, whereas this number has stayed firm in the current tape. And, importantly, this market has been making all-time highs for four years, staking a claim as a new “secular bull market.” The new highs in mid- to late-’07 were barely above the March 2000 levels of the prior bull market.

Asked what clues investors should’ve been focused on back in mid-2007 to have a sense of the poor risk-reward that lay ahead, Ned Davis Research chief U.S. equity strategist Ed Clissold says, “I would put recession warning signs at the top of the list: flattening yield curve, widening credit spreads, and falling earnings growth and profit margins.”

The yield curve – the spread between the two- and ten-year Treasury yields – has been a source of some angst recently, but at more than 0.9 percentage points is not even close to sending a loud alarm. In July 2016, it was barely above zero and had spent much of the prior 18 months “inverted,” with the two-year yield above the ten-year’s). That inversion is a classic (if often early, and not foolproof) harbinger of a coming recession.

Clissold points out S&P 500 corporate profits went from a 22-percent rise in third quarter 2006 to a 9 percent drop by the third quarter of ’07. Today, forecasts are firmly positive for the coming quarters, with a chance that we see a 10 percent gain for the most recent period.

Credit conditions were turning hazardous during the third quarter of 2007. The St. Louis Fed Financial Stress Index was starting to flare higher, whereas it now shows a near-record-low level of capital-markets stress. Junk-bond spreads are near their tightest levels of this cycle, while a decade ago they began surging dramatically.

Don’t forget, too, that oil prices soared from $60 to $130 between mid-2007 and mid-2008 – a brutal exacerbating factor as the U.S. economy succumbed to the housing bust and recession. Few signs of such a move are evident now.

The market is now adjusting to a Fed that seems intent to proceed a bit quicker with the process of “normalizing” rates from historic lows. Back then, the Fed had been on hold since mid-2006 after having ratcheted short-term rates higher 17 times over two years. It stopped as the economy slowed and the yield curve became flat. By September 2007, as the subprime mortgage crisis started rolling faster, it cut rates. Clearly, we are in a very different, and more favorable, spot today.

Things began to worsen pretty fast in ’07, and began when unemployment was at 4.4 percent and the ISM manufacturing index in the mid-50s (both close to current levels), so an all-clear can never be sounded. And today’s market is way overdue for a shakeout, correction, or at least a pullback of at least 5 percent – something we haven’t seen since October.

But the weight of the evidence argues pretty clearly against an imminent, devastating market downturn now – at least in part because we keep seeing articles inquiring about whether the top is near.

Source: Investment Cnbc

10 years after the last bull began to fail, this market shows fewer signs of trouble