Blue Apron is among the worst-performing IPOs year-to-date — and it’s only been one week.

That’s according to Kathleen Smith, principal at Renaissance Capital, a manager of IPO-focused ETFs.

“The trading on this has been just awful,” Smith said. “Some of it is the Amazon fear but that’s not the only thing. Some of it is the IPO market itself. Investors are jumpy around valuation.”

The “Amazon fear” stems from a merger between Amazon and Whole Foods, announced just ahead of Blue Apron’s public offering. The e-commerce giant beat out six other interested parties to buy the natural grocer, according to new details revealed in a proxy statement filed with the Securities and Exchange Commission.

Blue Apron, which delivers fresh ingredients for recipes, has been battling the headlines ever since, said David Seaburg, head of sales trading at Cowen and CNBC contributor.

“Although it’s a neat concept, the dominant players within the space will compete at a level that won’t allow Blue Apron to be successful long term,” Seaburg said. “It’s all about scale, it’s all about relevance. You look at Kroger, Whole Foods and Amazon. They can take this section of the market over from a price perspective alone in a very short period of time.”

Source: FactSet

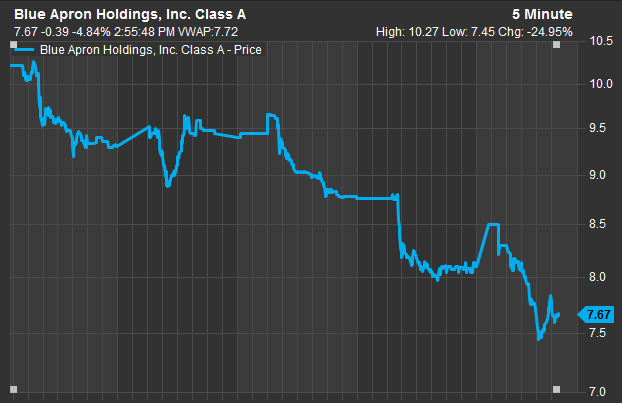

Shares of Blue Apron were down more than 4 percent on Friday afternoon, ending the week down 17 percent. At $7.73, the share price was far below the IPO price of $10 a share.

Blue Apron’s not the only recent IPO that had a tough first week: Tech company Tintri closed the week down nearly 6 percent, after going public last week, a hair lower than its IPO price.

“I think you saw the air come out of it when the price was reduced,” Seaburg said. “Because of the scare that Amazon put into the marketplace with their strategic move. … For any investors that have a long-term view, maybe the narrative has shifted.”

Both Tintri and Blue Apron lowered the expected range for pricing before going public. With a market capitalization of around $1.5 billion on Friday, Blue Apron traded at less than the $2 billion it was valued at by its backers in the private market.

It comes after a combination of busy activity in the venture capital market, paired with a dearth of IPOs over the past few years.

“There is a world of difference between a private valuation versus the public market, because there are so few involved in [the private market],” Smith said. “In this case, it’s a big disparity. It could be that the company expects certain things about valuation based on the sweet nothings whispered by their early investors. When you have a company that’s not making money, the anchor for its valuation is very weak.”

Still, Blue Apron isn’t the year’s worst performing IPO, Smith said. Indeed, Renaissance’s fund, which tracks IPOs, is just off all-time highs, as companies who went public earlier are stabilizing and doing well, Smith said.

Smith pointed to Facebook, which languished for months after its IPO. But Blue Apron’s valuation could weigh on other similar companies who are considering an IPO, Smith said.

“Whether the IPO price was right or not, these things have to work themselves out,” Smith said. “Markets have been much more subdued and institutional than in the past. Institutional investors are really picky about wanting to make money. …. At some point investors are going to take the other side of this trade.”

Disclosure: Cowen and Company, and or its affiliates make a market in the stock of Amazon.com securities.

Source: Tech CNBC

Blue Apron shares plunged more than 17% in their first week on the market