Active managers, rejoice.

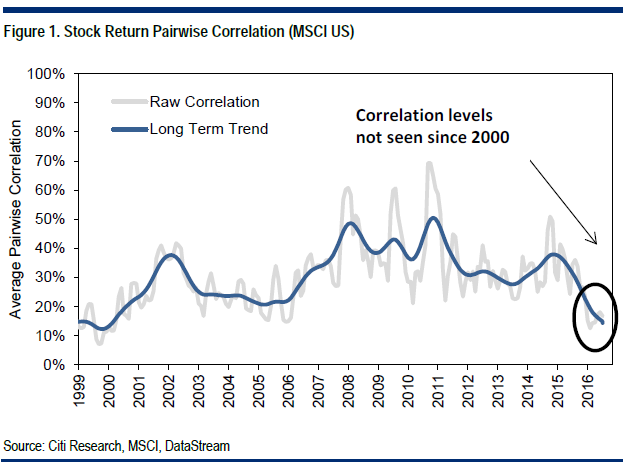

Analysts at Citi put together a chart that illustrates how the correlation among stock returns in markets like the United States is at its lowest level since 2000.

Here’s the chart:

“This should bode well for active management performance and indeed year-to-date, global active management performance for the median manager is positive,” Citi analyst Chris Montagu said in a note Monday. “With less stock return co-movement in global equity markets, the theory (hope) is that this would translate (or though not necessarily the cause) to a better environment for active stock selection.”

Active managers, or stock pickers, put up a strong showing in the first half of 2017. According to data from Bank of America Merrill Lynch, 54 percent of large-cap managers beat their benchmarks to start off the year. For the second quarter, 60 percent beat, marking the best quarterly performance since the first quarter of 2009.

That said, investors have also benefited from one of the least volatile markets in years. The CBOE Volatility Index (VIX), widely considered the best gauge of fear in the market, hit its lowest level in more than 20 years earlier this year.

“Whatever the explanation, looking forward equity volatility appears too low given potential [central bank] tightening, political risks, and stretched valuations together with some markets making new highs,” said Montagu.

Central banks around the world have their sights set on tighter monetary policy in the near future. This could shake up global markets as traders and investors scramble to reposition their portfolios.

Source: Investment Cnbc

This chart shows why this is the best 'stock pickers market' in 17 years