Energy stocks might be on course for another fourth quarter rally this year, in part because investors are too focused on negative headlines, according to Tamar Essner, senior energy director at Nasdaq Corporate Solutions.

“It kind of feels like deja vu of last year where energy underperformed for most of the year and then in Q4 rallied tremendously and we became the best performer in the year,” she told CNBC’s “Squawk Box” on Thursday.

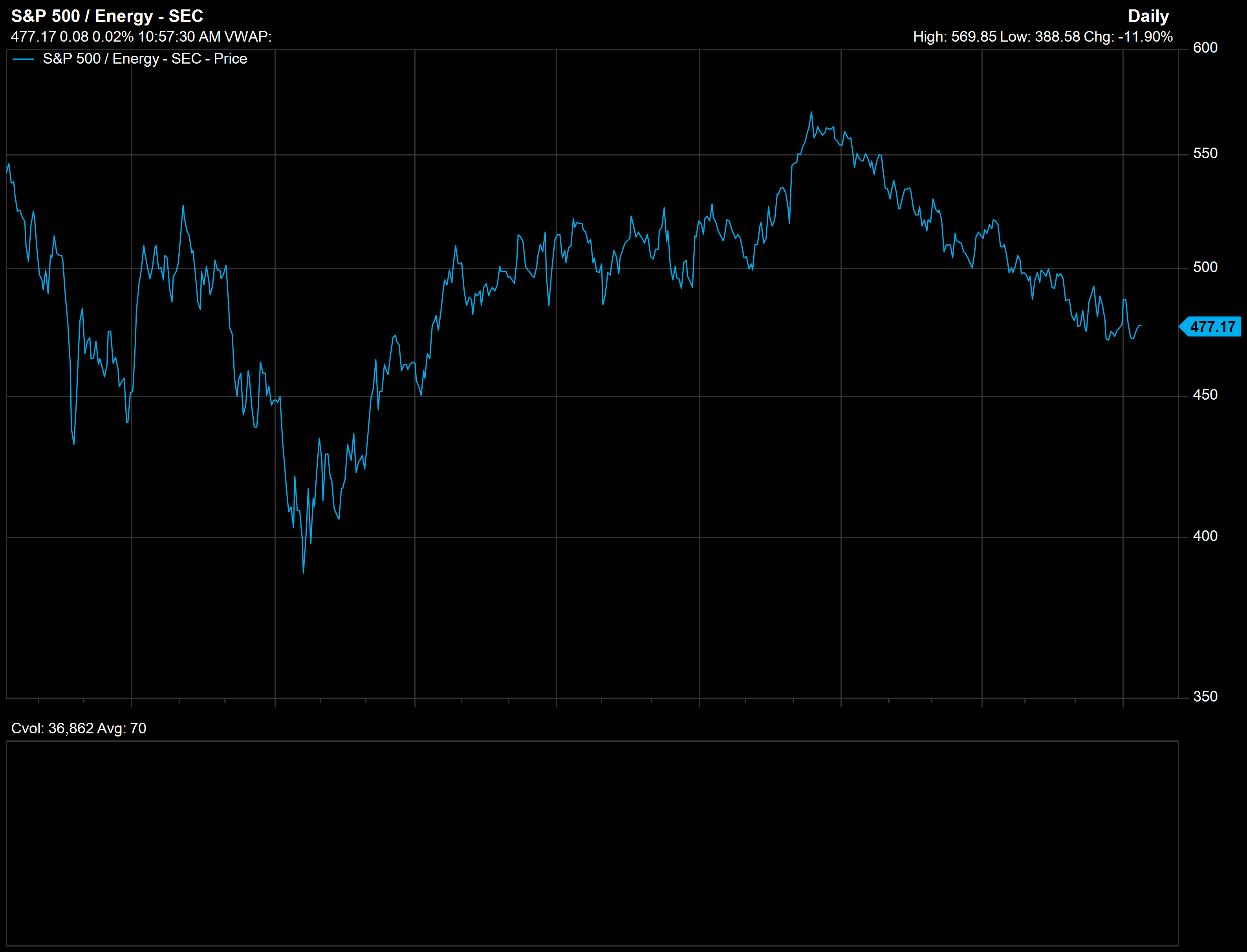

The S&P energy sector surged about 8 percent in the final three months of 2017, dovetailing with a rise in oil prices as OPEC hammered out a deal to cut crude production.

S&P energy sector two-year performance

But the sector’s fortunes have turned as oil prices sputter against a backdrop of rapidly rising U.S. production and concerns about OPEC’s ability to end a crude glut. The S&P energy sector is down more than 14 percent this year, making it the second worst performing sector after telecommunications.

Essner did not guarantee the same late-year surge for energy stocks, but presented the bull case for the sector.

On the commodity side, rising output from the United States and OPEC members Nigeria and Libya has created a negative confirmation bias, in her view.

“Anything that’s positive in the market gets overlooked, and we focus in on these negative data points,” Essner said.

She noted that bearish bets on crude oil have recently risen while may traders have unwound wagers that prices will rise. That typically makes it harder for bears to push prices lower and increases the risk oil futures will tick higher. While oil prices will likely remain stuck in a range between $40 and $50 a barrel this year, the risk is now to the upside, Essner said.

The credit market also remains relatively open to drillers seeking to fund production even as energy stock prices have tanked, Essner added. That’s important because 20 to 25 percent of U.S. oil output depends on access to the high yield debt, she explained.

To be sure, U.S. production growth would take a hit if credit markets tighten, she said.

On Wednesday, Goldman Sachs‘ head of commodities research Jeff Currie told CNBC it has become difficult to predict how high oil prices need to be in order for oil companies to profit from drilling new wells. That is in part due to ample funding from private equity firms, which allows drillers to start up new production despite low prices.

Some U.S. shale drillers can break even on new production with oil prices below $20 a barrel, according to Essner. She said there is a clear link between private equity funding and rising U.S. output.

“Where the rig counts have really been going up is in the rigs that are backed by the private equity money,” she said.

Source: Investment Cnbc

Energy rally 'deja vu': Why oil stocks could stage another late-year surge