A million barrels of oil doesn’t buy much good will these days.

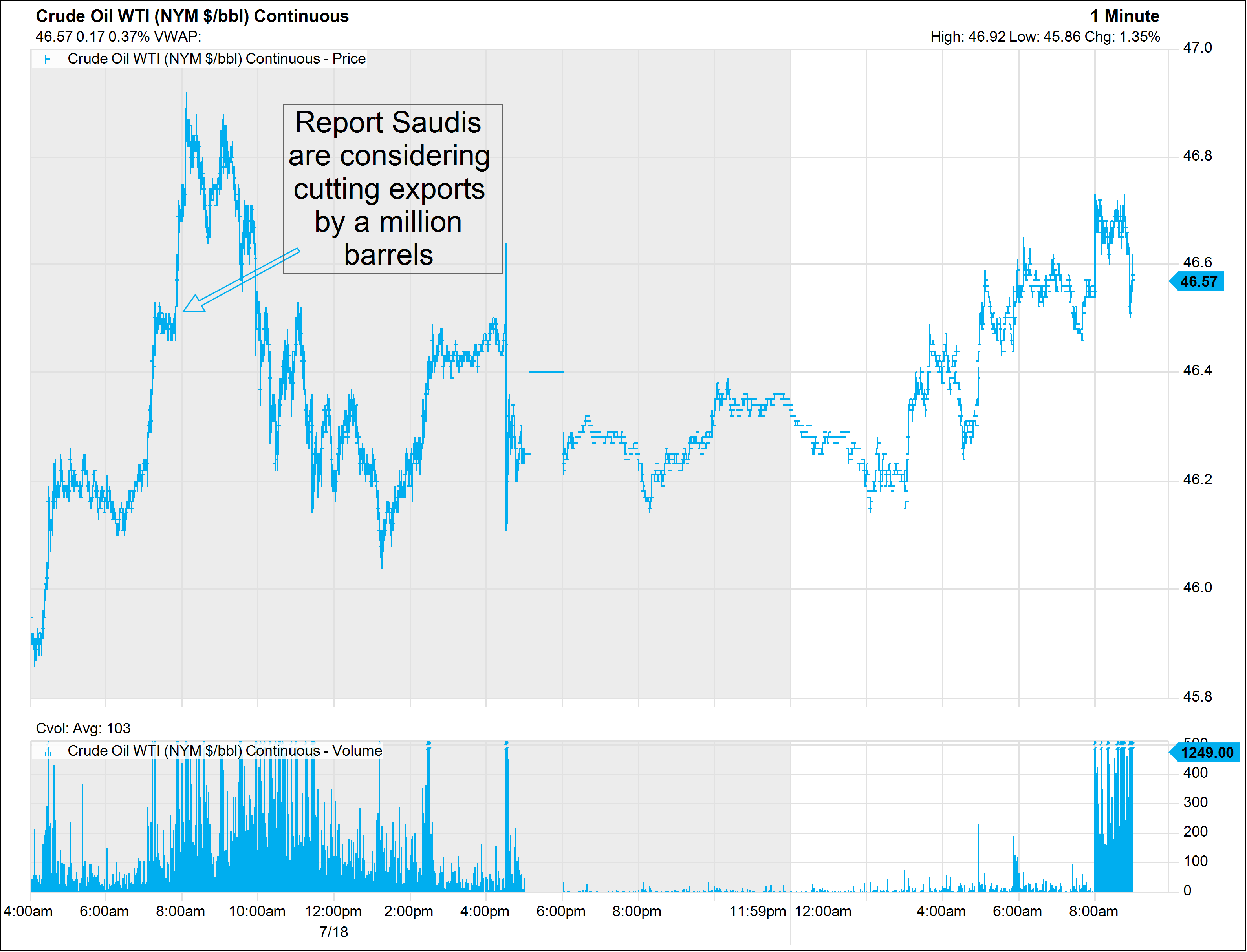

Oil markets got a temporary boost on Tuesday on reports that Saudi Arabia could cut its crude exports by a further 1 million barrels. It was the kind of news that could once sustain a session-long surge, but almost as quickly as futures popped, the rally fizzled.

U.S. crude prices then spent much of the session bumping around barely positive territory, eventually grinding 38 cents higher to settle at $46.40 — comfortably within the $10 range the contract has traded in for nearly three months.

WTI crude was just 23 cents higher to $46.82 midmorning Wednesday New York.

U.S. West Texas Intermediate crude

On its face, the report was exactly what the market has been awaiting. Despite OPEC‘s deal to cut the number of barrels it produces, exports haven’t fallen in lockstep. So while Saudi Arabia and its cohort are pumping less oil, much of it is still finding its way to foreign storage tanks, undermining the cartel’s goal of shrinking huge global stockpiles.

The message from the market is clear, say analysts: show me the barrels.

“You’d really have to prove it to them. They’ve seen mixed signals,” said Tom Kloza, global head of energy analysis at Oil Price Information Service.

The potential export cut basically balanced out an earlier report that Saudi Arabia’s production rose in June, Anthony Grisanti, founder of GRZ Energy, told CNBC’s “Futures Now” on Tuesday.

Last week, Saudi Arabia reported it had slightly exceeded the production cap it agreed to last winter, when exporters struck a deal to cut their combined output by 1.8 million barrels a day.

Before that, tanker tracking firms said Saudi crude export loadings spiked in June after a long-awaited plunge in April. Around the same the exports rebounded, reports emerged that Riyadh was cutting shipments to U.S. ports and paring back August exports by 600,000 barrels a day to the lowest levels this year.

Tuesday’s brief rally on yet another Saudi export signal may have sent prices toward recent highs, but traders took the money off the table in short order, said Tamar Essner, director of energy and utilities, at Nasdaq Corporate Solutions. That fits with a common theme in recent weeks: oil prices may pop on a bullish headline, but the gains will evaporate unless the news is backed by data.

“Today’s story was that the Saudis are merely considering further export cuts, but this hasn’t materialized yet and what we do have hard data on shows that Nigerian and Libyan exports are up, in defiance of expectations,” she told CNBC on Tuesday.

The market remains skeptical about deeper cut to Saudi exports, especially one so large that doesn’t have clear support from fellow OPEC members, Essner said. That skepticism is justified given that Saudi Arabia has continued to aggressively pursue Asian business to maintain market share in the key demand center, she added.

A million-barrel-a-day drop in exports would certainly have an impact on the market, Kloza said, but it would be tough to get other OPEC members to follow suit.

The Saudis “have the power to certainly influence the market, but you have to wonder about the motivation,” he said.

Correction: Saudi Arabia’s production rose in June. An earlier version misstated the month.

Source: Investment Cnbc

Oil market shrugs off potential Saudi export cut as traders tire of 'mixed signals'