ACCORDING to company lore, Yunnan Baiyao, a musty-smelling medical powder, played a vital role during the Long March. As China’s Communist troops fled from attacks in the 1930s, trekking thousands of miles to a new base, they spread its yellow granules on their wounds to stanch bleeding. To this day, instructions on the Yunnan Baiyao bottle recommend application after being shot or stabbed. Many Chinese households keep some in stock to deal with more run-of-the-mill cuts. But the government has recently put its maker into service to treat a different kind of ailment: the financial weakness of state-owned enterprises (SOEs).

Yunnan Baiyao has emerged as a poster-child of China’s new round of SOE reform. The company, previously owned by the south-western province of Yunnan, sold a 50% stake to a private investor earlier this year. The same firm had tried to buy a slice of Yunnan Baiyao in 2009 but was blocked. Its success this time has been held up in the official press as proof that a push to overhaul sluggish state companies is at last gaining momentum under Xi Jinping, China’s president.

-

Climate change might prevent airlines from flying full planes

-

Why yurts are going out of style in Mongolia

-

Conservatives speak louder in secular France than in pious Germany

-

Jordan Spieth′s Open victory illustrates the perils of playing it safe

-

Donald Trump’s spokesman quits

-

Turkey’s growing repression leads to a showdown with Germany

But for many investors and analysts, the Yunnan Baiyao case proves just the opposite: that SOE reforms are stuck in a rut. The sale, after all, left half the company in state hands. And a traditional Chinese medical powder is far removed from industries such as energy and finance, which the government deems strategic and is less willing to open to private capital.

It is hard to overstate the importance of getting SOE reforms right. In the 1980s, when China was starting to open to the world, the state sector dominated its economy, accounting for nearly four-fifths of output. A big factor behind China’s remarkable growth since then has been the relative decline of SOEs, to the point that they account for less than a fifth of output today. As state firms stood still, a vibrant private sector sprouted around them.

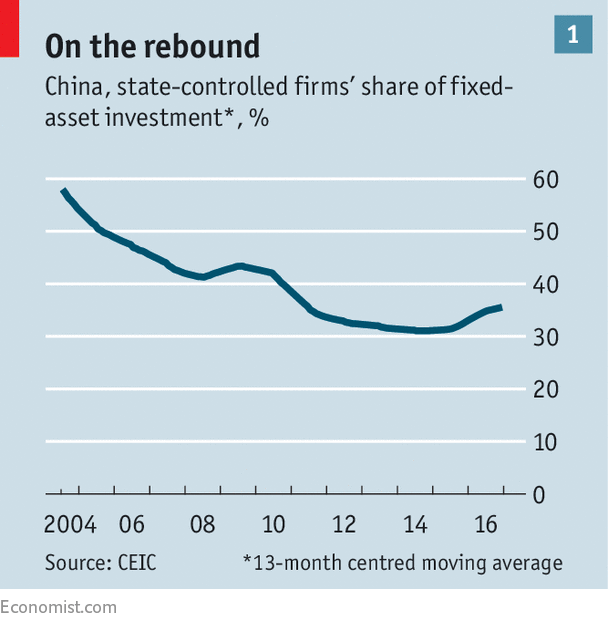

Over the past few years the state sector has, by several measures, stopped shrinking. There are still more than 150,000 SOEs in operation, two-thirds owned by local governments and the rest under central control. Private firms are much more productive, but state firms gobble up a disproportionate share of resources. They take about half of all bank loans and are the main culprits behind China’s big increase in corporate debt. Since 2015 investment by SOEs has grown faster than private-sector investment, reversing a decades-long trend (see chart 1).

For China this has the makings of a damaging cycle. As growth slows, the government leans on SOEs to spend more; but this drives up their debt further and so weighs on the economy. Putting a stop to this sequence is vital for China if it is to become wealthy. The IMF estimates that an ambitious programme of SOE reform could expand the Chinese economy by nearly 10%, or about $1trn, over the next decade.

The fate of China’s state firms is also a global concern. By international standards, they are already massive. China’s 200 biggest SOEs account for 18% of global revenues of integrated oil and gas companies, 6% in carmaking and 5% in construction (see chart 2). A series of mega-mergers currently under way is concentrating even more power in the hands of a few, giving them the heft to barge into new markets. For foreign firms this can smack of unfair competition, as if they are fighting against the Chinese state. The temptation for other countries to block foreign investments by SOEs will only increase, setting the stage for bitter disputes.

Market failure

Back in 2013 Mr Xi seemed to grasp that change was needed. He vowed that market forces would play a “decisive role” in allocating resources and declared that reform of SOEs was a priority. Although a big-bang privatisation was never on the cards, the hope was that the government would make SOEs better run, more competitive and less coddled. There has been a bewildering array of directives and pilot programmes since then but little real progress. The fear is that the reforms, taken together, not only fail to solve the most pressing problems, but might even be aggravating them. SOEs are getting bigger, not smaller; their management has become more conservative; and their deficiencies are beginning to infect the economy more widely.

Keeping track of all the different experiments that fall under the heading of “SOE reform” is a full-time job. When Mr Xi put it on the agenda in 2013, the government broke it down into 34 separate initiatives, farmed out to different departments and agencies. It has since published at least 36 supplementary documents and launched reform trials at 21 different firms. Provinces and cities have followed up with dozens of plans, guidelines and trials of their own.

Some promising ideas are afoot. After years of discussion, China has started to let state firms award shares to employees as part of their pay packages. SOEs had tried such schemes in the 1980s and 1990s, but the government stopped them, fearing that senior executives were siphoning off state assets, much like Russia’s oligarchs.

Shanghai International Port Group (SIPG), a city-owned firm, is one of the companies pioneering employee ownership of shares. It also demonstrates how local SOEs, though smaller than their national peers, are often huge themselves: SIPG is the principal operator of Shanghai’s cargo port, the world’s busiest. In June 2015, as a first step, it allocated 1.8% of company shares to employees; some 16,000 of its 22,000 employees now hold a stake. Ding Xiangming, vice-president of the port group, believes he is already seeing results. “Workers are more focused on our company’s growth,” he says.

Public and private

Shanghai is also an example of how parts of the country can outpace others in SOE reform. Last August the People’s Daily, the Communist Party’s main newspaper, hailed the city as a model for other local governments. Shanghai moved quickly to classify its SOEs as either commercial (eg, SAIC Motor) or in public service (eg, Shanghai Metro). This is a distinction that the central government wants to see applied nationwide, so that companies classified as commercial can be treated more like private firms. Shanghai’s commercial SOEs have more leeway to hire managers from the private sector and to pay market rates.

Another potentially promising idea is “mixed-ownership reform”, a fancy term for allowing SOEs to sell stakes to private investors, as in the case of Yunnan Baiyao. The thinking is that private shareholders will demand more from SOEs, especially if their investment is combined with a seat on the board. As a concept it is not new: many big SOEs have been listed on the stockmarket since the early 2000s, attracting outside investors. But Cao Zhilong of Shanghai United, a law firm, thinks this round of mixed-ownership reform could lead to bigger deals: “The word privatisation is not used. It is too sensitive. But the state can sell a majority.”

At national level, the mixed-ownership trials have been disappointing. The state is mainly selling minority stakes in the subsidiaries of large groups, such as a 45% share in the logistics arm of China Eastern Airlines, a deal completed in June. But for local SOEs, outright sales are easier. Tuopai, a small town in Sichuan, sold a majority stake in its struggling liquor company to a Chinese private-equity firm last year. The change in culture is already apparent. The company has rolled out slick new adverts and uses designer bottles instead of the old ones with ill-fitting labels. It has also cut about a third of production staff to make way for more automation, the kind of unpopular decision that a government-owned company is loth to make.

In general, though, such deals are rare. This cannot just be blamed on the government; a basic dynamic is also at work. “Profitable SOEs don’t want to sell to outsiders and no one wants to buy a struggling SOE,” says Hong Liang of Everbright Law.

What can be blamed on the government are conflicting messages. Less noted at the time of Mr Xi’s 2013 pronouncement about market forces, but more glaring now, was his declaration that SOEs should continue to play a dominant role in the economy. The implication is that he wants state firms to be better run—hence the emphasis on the market—but only so that they better serve the party by helping it to manage the economy at home and carry China’s flag into foreign territory. Mr Xi has made this point in increasingly strident terms. At a meeting on SOEs last October he devoted his comments not to reform but to the necessity of strengthening the party’s grip. “The party’s leadership of SOEs is a major political principle, and that principle must be insisted on,” he said.

People who work in and with SOEs report a palpable change in atmosphere in recent years. “Party officials are not the same as the technocrats who used to run the SOEs,” says a top banker. “They don’t take risks. Doing nothing is what’s safe.” Some of the most capable employees are leaving SOEs altogether. Political education, always a part of life in state firms, has been stepped up. One manager who recently quit a big state bank said that a campaign exhorting workers to study the party constitution had been unusually intense.

At the same time the government has capped pay for senior executives, concerned that they were getting more than government employees of equivalent ranks, stoking resentment. Yet on an international basis, SOE bosses are dramatically underpaid. The president of PetroChina, the country’s biggest oil company, earned 774,000 yuan ($112,000) in 2016; the CEO of Chevron, a firm of roughly the same market value, pulled in a handsome $24.7m.

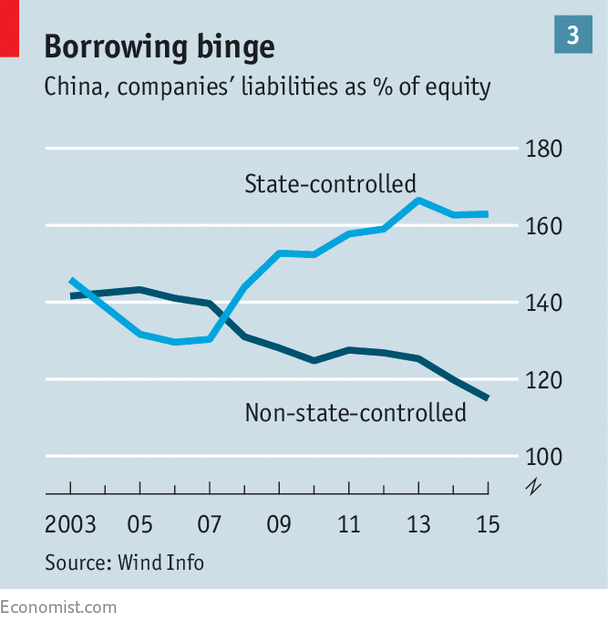

Signs suggest that after seeing morale suffer without any improvement in performance, the party is rethinking at least some of its policies. A senior official in charge of supervising SOEs said in June that it would be wise to delegate power to company boards, giving them more say over long-term planning and hiring decisions. Li Keqiang, China’s prime minister, told a meeting of 100 leading executives in April that the government might try to implement a system of performance-linked pay at big state firms. At a conference on July 15th, Mr Xi said it was vital that SOEs reduce their excessive debts (see chart 3).

But Mr Xi’s emphasis on party leadership has also created cover for those seeking to defend and even expand state power. The most important role in this is played by SASAC, the arm of the government that oversees most SOEs. It has pushed for the creation of bigger “national champions” under its control. It has combined China’s two biggest railway-equipment makers and its two biggest shipping groups, and is reportedly working to knot together its two biggest chemical producers. Medium-sized companies, too, have seen plenty of such activity, affecting property, ports, cement and more.

Some mergers make sense: for instance, the steel sector is highly fragmented, a result of local protectionism. But most combinations look more dubious, because state firms are already oversized. The average SOE has about 13 times more assets than the average private-sector firm, according to World Bank estimates. What is more, in many industries, the only competition faced by state firms is from other state firms. Indeed, part of the rationale for the mergers is to prevent SOEs from butting up against each other as they go abroad to win business, as had happened with railway-equipment makers.

In the 1990s, when SOE reforms began, the vision was of the state controlling whole industries but with the companies in them battling each other to promote better management. The imperfections of this scheme are clear, judging by weak returns in the state sector. But the government’s response is to create even bigger monsters. Chinese economists have described them as “red zaibatsu”, a reference to Japan’s sprawling, slow-moving conglomerates. Yanmei Xie of Gavekal Dragonomics, a research firm, is even blunter: policymakers “are trying to create conglomerates that can dominate domestic and international markets through sheer size”.

The risk is that such supersized SOEs could hurt the global economy. In a paper published earlier this year, Caroline Freund and Dario Sidhu of the Peterson Institute of International Economics, a think-tank, argued that businesses around the world were operating in more fragmented environments, with the exception of sectors in which Chinese SOEs have large footprints. In these sectors, such as mining and civil engineering, concentration has increased as China’s state firms have bulked up. Normally, it is the most productive companies that grow the fastest. China’s SOEs, by contrast, are much less efficient than their international counterparts, even when they are growing more quickly, according to Ms Freund and Mr Sidhu.

The business of state

The saving grace in the past was that the vast majority of SOE business was within China. That is changing: industries from construction to steel to railways are looking abroad. The “One Belt, One Road” strategy—the core of Mr Xi’s foreign policy—has made foreign expansion an explicit part of their mandate. The danger is not just that they will elbow Chinese private-sector competitors aside but that in doing so, they will provoke a backlash. Big firms in other countries will demand state backing in order to level the playing field. Foreign regulators, already wary of Chinese capital, will turn more hostile. The drift away from free trade could easily gather steam.

This is not the only worry. One of the keys to China’s economic rise hitherto has been its success in restricting the sprawl of state firms. They control the commanding heights of the economy, from transportation to power, but have largely been confined to these sectors. Hard-charging entrepreneurs have been free to break into new businesses around them. The manufacturers that led China’s export assault on global markets were private. The tech firms that dominate the internet are private. The restaurants, cafés and shops that line city streets are private.

Can anything cure China’s SOEs?

Can anything cure China’s SOEs?

This model still works, for now. Within the MSCI index of large listed Chinese firms, the state accounts for more than 80% of market capitalisation in sectors such as energy, industry and utilities, according to Morgan Stanley. But the state accounts for 40% or less of market value among consumer, health-care and IT companies, says the bank. With these newer sectors growing far more quickly than smoke-stack industries, private companies may well continue to outflank SOEs.

There is a big looming worry, however. One aspect of SOE reform is in fact making quick progress: the creation of what are known as “state capital investment and operation” companies (SCIOs), to help manage existing state assets and invest in new ones. This initially looked like part of the solution for China. It borrows an approach honed in Singapore, where Temasek, a government-owned holding company, manages a portfolio of state firms but does not meddle in their operations, apart from demanding that they deliver good returns. It is now clear that this is not what China has in mind. Government officials say that SCIOs should not seek to make money in their investments; rather, they are meant to be more like “policy funds”, seeding firms and industries with government cash or money raised from SOE dividends without worrying about profit.

The other striking feature of SCIOs is that they are expressly enjoined to break into new high-tech sectors. Provincial governments around the country have published plans over the past two years in which they promise to guide more than 80% of their funds into infrastructure, public services and, crucially, “strategic emerging industries”, a category that refers to new energy, biotechnology and IT, among other areas. The upshot is that SCIOs, armed with cheap capital, seem set on expanding the state’s reach into the private sector. “We should anticipate the emergence of literally thousands of well-resourced SCIOs,” says Barry Naughton at the University of California in San Diego.

State-backed private-equity funds, which can be seen as forerunners to the investment function of the SCIOs, are already making a big impact. To give three examples from last year: the city of Shenzhen launched a 150bn yuan fund; Jiangxi, a relatively poor central province, created a 100bn yuan fund; and the city of Chengdu set up a 40bn yuan fund. This influx of cash is pushing up valuations. Bain & Co, a consultancy, calculates that private-equity deals in China were priced last year at a frothy 26-times earnings before interest, tax, depreciation and amortisation, compared with ten times in America. The state may turn out to be a wise investor but experience suggests otherwise. More likely, the state will crowd out private investors, hogging capital and allocating it poorly.

The outcome does not have to be this bleak. Optimists still think that Mr Xi could spring a surprise after a big Communist Party congress later this year. With his authority firmly entrenched, he might feel emboldened to unleash the market forces that he spoke of four years ago. But based on his rhetoric and actions so far, this looks like wishful thinking. SOEs, far from retreating, are on the march, drawing on government support to compensate for their weakness. They are making conquests at home and abroad. Cutting state firms down to size and opening them up to competition ought to be the point of SOE reform. Instead, China is beefing them up and driving them into new territory.

Correction (July 20th): This article and the second chart have been amended to remove references to integrated oil and gas companies because the figures we used are skewed by the exclusion of large non-listed firms such as Aramco of Saudi Arabia

Source: economist

Reform of China’s ailing state-owned firms is emboldening them