Carl Icahn‘s bet on an obscure biofuel credit is going south and threatens to leave an energy company he controls with a big unpaid bill.

The wager is remarkable because Icahn’s role as a special advisor to President Donald Trump has directly influenced the price of the credits he is betting on. The fact that Icahn’s gamble is going bad is due at least in part to his inability to convince the Trump administration to change a policy that disadvantages one of his investments.

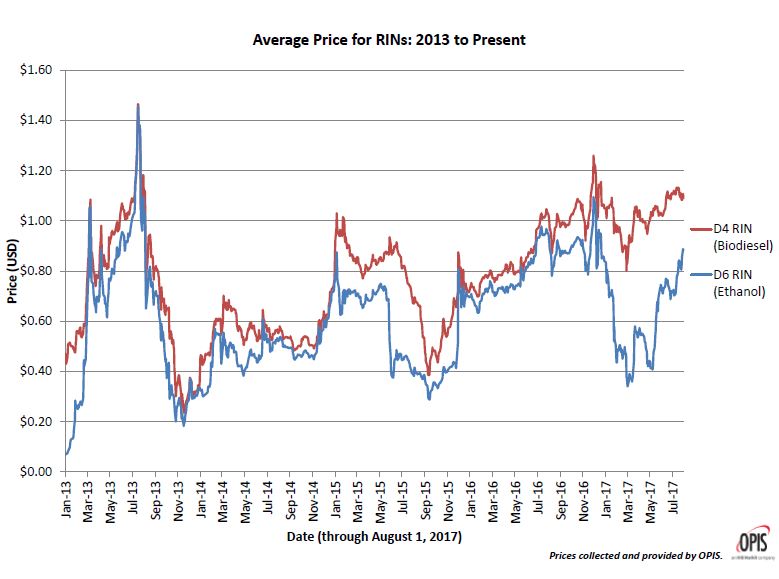

Icahn was betting the cost of the biofuel credits would fall, and initially it did. But through Aug. 1, the credits have rallied nearly 200 percent from the February low.

As a result, CVR Energy, the company through which Icahn is making the bet, has booked a nearly $280 million liability. If things keep going this way, the liability could eat into CVR’s cash pile, leaving it with less money to distribute to shareholders. That would likely dent CVR’s stock price, which is down 25 percent this year [though it is still up 35 percent over the past 12 months.]

The policy Icahn hoped would change requires companies that refine fuel to blend biofuels such as corn-derived ethanol into gasoline. Refiners that meet their obligation generate credits called renewable identification numbers, or RINs. They sell those credits to smaller merchant refiners that don’t have the capacity to blend biofuels into gas.

Icahn’s strategy concerns some analysts who cover CVR Refining, the Sugar Land, Texas-based refiner controlled by CVR Energy.

CVR Refining “is managing its RIN obligations far differently than other U.S. refiners,” said Chi Chow, an analyst at energy investment bank Tudor Pickering Holt, referring to the biofuel credits.

“Sustained lower RIN prices may produce a cash windfall that could be used to ramp distributions, but any material increase in prices could push its liability even higher,” he wrote in a research note.

Chow wrote that note in May, just as the tide started to turn against Icahn.

Former President George W. Bush’s administration created the Renewable Fuel Standard to reduce American dependence on foreign oil shortly before U.S. crude output started booming.

The system inherently disadvantages merchant refiners like CVR, in which Icahn Associates holds an 82 percent stake. Icahn has long called for the requirement to blend biofuels to be scrapped. He argues that speculators drive up RIN prices, putting small refiners at risk of bankruptcy, which raises concerns about U.S. energy security.

More recently, Icahn has advocated for passing the burden of mixing ethanol onto fuel blenders, which would let CVR off the hook. This is called changing the “point of obligation” in industry jargon.

RIN prices fell last winter after Trump announced he would nominate Oklahoma Attorney General Scott Pruitt, a longtime fossil fuel ally, to lead the Environmental Protection Agency, fueling speculation that the EPA would change the Renewable Fuel Standard in a way that would benefit refiners. RIN prices fell further after Trump announced Icahn would advise him on regulatory policy.

Changes in RIN prices reflect the market’s outlook on how many of the credits refiners will need to buy. In the first part of the year, the market was betting demand was going to dry up. CVR appeared to be making the same bet, according to Chow.

“[M]anagement is clearly speculating on the price of RINs — a practice that they heavily criticize as a reason why the market is so apparently manipulated,” he said in his May note.

While CVR does not offer much detail on its RIN purchases, analysts say it appears that the refiner stopped buying the credits last year, and perhaps even sold some — a strategy that would pay off if RINs prices fell.

“[T]he proportional growth in the current liability over time suggests that the company has purchased few, if any, RINs to cover the obligation incurred since” the second quarter of 2016, FBR Capital Markets analyst Benjamin Salisbury wrote in a recent research note.

Not buying RINs is like running up a bar tab — that is, if the cost of beer fluctuated wildly and your final bill was calculated based on the price of suds on the day you settle up.

The EPA allows refiners to run a deficit for a while, but they must eventually meet their full obligation. CVR was essentially betting it could buy up cheap RINs before a deadline to meet its obligation in the first quarter of 2018.

CVR declined to comment for this story. Icahn Associates did not respond to a request for comment.

Icahn acknowledged in March that CVR was delaying its RIN purchases for a year, which is allowed under the program.

“I’m not selling ’em, I’m not buying ’em,” Icahn told Bloomberg. “Hey, this is what I do in the market. I’m taking a chance.”

Icahn said the bet is about beating speculators. He maintains that he is only an informal adviser to Trump and the president is under no obligation to take his advice. He is not a government employee so he is not required to divest his assets — an arrangement that some call a conflict of interest.

Icahn’s wager initially went his way, with RINs falling as low as 30 cents in the first quarter, 34 cents below the lowest level in the year-ago period. They struck the low following a report that a U.S. biofuels trade group backed Icahn’s plan, and that the deal was being sent to Trump.

“That was an Icahn drop,” said Tom Kloza, global head of energy analysis at Oil Price Information Service.

But the market made a critical error in assuming the deal between Icahn and the trade group would bear fruit at the EPA, Kloza said. A little research showed that it was unlikely that Trump and the EPA would execute Trump’s plan, he said. It would have made the regulation more complicated and exacted a political toll in corn-producing parts of America that voted Trump.

“That whole notion that they would change the point of obligation and it would change immediately, that was so flawed,” Kloza said. “Saying it was flawed was like saying the Pacific Ocean is moist.”

The market may have also been overestimating the impact of Icahn’s plan to change the point of obligation.

Shifting the responsibility for blending ethanol away from refiners and onto blenders would have changed who is responsible for buying RINs, but it would not have significantly transformed supply and demand for the credits, said Andy Lipow, president of Lipow Oil Associates.

“There are a lot of people participating in this market that don’t understand the underlying regulations,” he said.

By May, it began to appear that the EPA would leave the amount of biofuel refiners were required to blend into gasoline mostly unchanged in 2018. RIN prices began to rise steadily, bumping higher as the EPA indeed proposed keeping levels steady.

Later that month, a federal appeals court ruled the Obama administration had erred by setting blending levels below previously determined levels. That raised concerns blenders would have to buy more RINs, further supporting prices. CVR Energy’s stock fell about 8 percent and CVR Refining shares tanked more than 15 percent in one day.

Last week, reports surfaced that the EPA would not take Icahn’s suggestion to shift the burden of buying RINs from refiners to blenders.

That cut off the primary path for Icahn’s bet to pay off. This comes as CVR Refining reported a liability of $279.9 million tied to its biofuel blending obligation through the second quarter.

That obligation jumps to $321.6 million based on the recent high RINs price of 88 cents, FBR Capital Markets calculated in a research note. If CVR does not start covering its RIN obligation, its liability could balloon to $390 million, the investment bank said.

To be sure, RIN prices could yet fall, shrinking CVR’s liability, if it gets regulatory relief from EPA on another front, or if market conditions change.

Kloza, however, believes RIN prices have likely reached stasis around the 90-cent level, and Lipow believes they could head higher from Friday’s prices around 86 cents.

“Based on the renewable fuel standard of 2017 and 2018, I expect that RIN prices are going to be drifting up during the course of 2017,” Lipow said.

Source: Investment Cnbc

Here's how Carl Icahn's bet on Trump's energy policy went terribly wrong