Volatility in the Treasury market has sunk to a multidecade low, and that could have sweeping implications for the bond market this year.

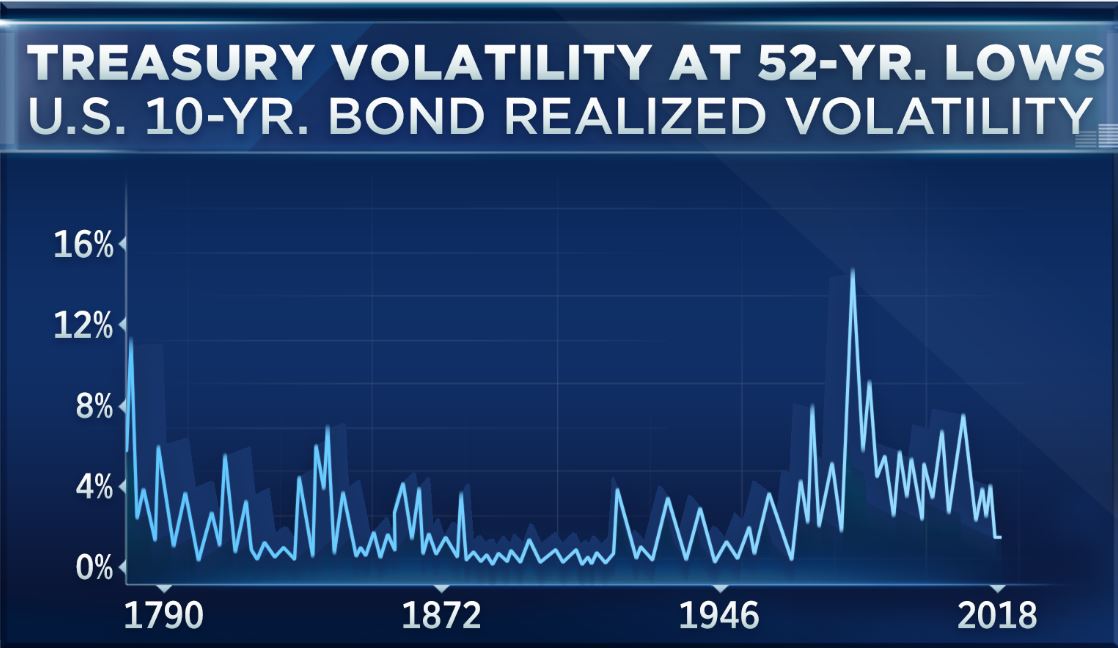

Treasury volatility as measured by realized volatility in the U.S. 10-year Treasury note has fallen to a 52-year low, according to a new report from Bank of America Merrill Lynch. I believe this is going to open the door to an inverted yield curve, wherein the longer-dated Treasuries carry a lower yield than those that are shorter-dated; this development is classically taken as a troubling signal for the broader market.

Indeed, we have already seen a stunning flattening in the yield curve as measured by the spread between the 10-year and 2-year Treasury yields. Furthermore, the 10-year yield has failed to take its high from the first quarter of 2017, and the 30-year has remained even more contained in its moves.

Ultimately, these long periods of muted moves will lead to a mean reversion. As a futures trader, I watch the Treasury futures, which trade in prices (which move inversely to yields). At this point, I anticipate volatility will pick up in the coming months and that the 30-year Treasury prices will rally at a faster clip than the shorter-end — the 2- and 5-year Treasury yields.

Think about it this way: As prices in the 30-year rise, the yields in the 30-year will sink. As the Federal Reserve tightens monetary policy, the shorter-dated bond yields will go through their own periods of containment. Theoretically, this should encourage the 30-year Treasury yield to fall beneath that of the 2- and 5-year.

So, how should investors position themselves if we are expecting this kind of price action across the bond market?

Investors ought to sell three 5-year Treasury futures contracts for every one 30-year Treasury futures contract bought.

The bond market is doing something it hasn’t done in 52 years