WHEN Caronte & Tourist, a Sicilian ferry company, needs a new ship, it is cheap and easy to borrow from a bank. But in 2016, when Caronte’s controlling families wanted to buy back the minority stake held by a private-equity firm, banks balked at the loan’s unusual purpose. Edoardo Bonanno, the chief financial officer, also worried that the €30m ($33m) in extra bank debt might make shipping loans harder to obtain from them in future. So he turned instead to a direct-lending fund run by Muzinich & Co, an asset manager.

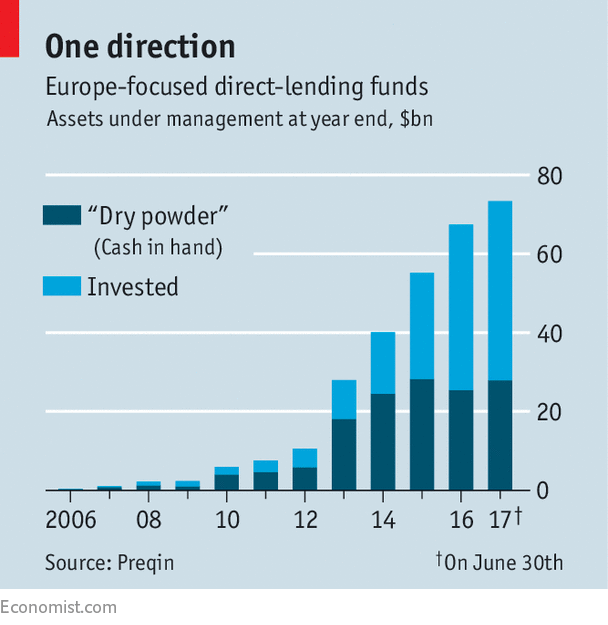

Such funds are only about a decade old in Europe (and not much older in America, where they started). Assets under management at Europe-focused funds increased from a mere $330m at the end of 2006 to $73.3bn by mid-2017, which includes $27.9bn of “dry powder”, or funds yet to be lent out (see chart). In 2017 alone 24 direct-lending funds raised a record $22.2bn. Such funds do what they say on the tin: lend directly to firms, usually in the form of big, multi-year loans. The borrowers are often either companies that are too small to raise equity or debt on capital markets, or private-equity funds buying such firms.

-

Some hotels charge visitors for bad reviews

-

Paul Romer quits after an embarrassing row

-

Music will miss irascible, unpredictable and prolific Mark E. Smith

-

Five English teams are among the ten highest-earning football clubs

-

Remembering Ursula Le Guin, the true wizard of Earthsea

-

Retail sales, producer prices, wages and exchange rates

Blair Jacobson of Ares Management, an asset manager, says that the pummelling banks took in the global financial crisis “turbocharged” the direct-lending industry. Ares set up its European direct-lending arm, now one of the largest with $10.8bn under management, in September 2007, as the crisis broke. Most of the other direct-lending firms moved into the business because of the crisis and the dearth of bank credit that ensued. Some were founded expressly for direct lending, notably Hayfin Capital Management in 2009, which in 2017 raised more than €3.5bn.

Despite superficial similarities, these firms are far from being banks. Many started out in more complex credit markets. ICG, for example, specialised in the riskier tranches of loans to private-equity firms. Another, BlueBay Asset Management, started as a bond-fund manager.

Direct lenders raise money from institutional investors, to whom they usually promise returns of around 10% or even 15%. So they cannot compete with the interest rates banks charge borrowers. But they do offer speed and flexibility. In Caronte’s case, for instance, Mr Bonanno liked the flexibility of Muzinich’s loan, such as the ability to pay it back early. The largest direct lenders, like Ares or Hayfin, can also compete on their ability to write large loans, even for several hundred million euros, off their own bat. Since the financial crisis, banks’ lending limits have been reduced, and syndication to even a dozen others can be like “herding cats”, in the words of Hayfin’s Andrew McCullagh.

Direct-lending funds also differ from banks in how much of their lending goes to private-equity firms. More than four-fifths involves private equity in some way, whether to finance a buy-out or to lend money to a private-equity-owned firm.

But that is changing. Many funds have formed ties with firms that become repeat customers when they need more financing. And direct lending is becoming better known as a financing option. For certain funds, a sizeable portion of their lending now has no private-equity “sponsorship”— about 40% for Hayfin, for instance, a third for Muzinich, and nearly half in Muzinich’s separate (albeit small) Italian fund.

The industry is also expanding geographically. As recently as 2013, Britain accounted for almost half of direct-lending deals; transactions elsewhere were often done by fund managers jetting in from London. But many European countries have allowed funds to lend without a full banking licence. And the EU plans to harmonise the direct-lending market. In the first three quarters of 2017, Britain’s share of new deals fell to a shade over a third. Many firms have set up regional offices, or even country-specific funds such as Muzinich’s Italian, French and British funds.

Direct lending covers a broad spectrum of activity. At one end is Muzinich, with its strong focus on small enterprises. This is a far cry from Ares’s boasts of being able to lend €300m at short notice (although Ares does lend to smaller firms, too). Yet both are part of a continuing structural shift in Europe, as a result of which small and midsized firms have a viable alternative to banks as a source of credit.

Source: economist

Direct-lending funds in Europe