For the past 10 years, the investment story on Apple was fairly straightforward.

Investors and analysts only cared about how many iPhones it sold.

And while that’s still the primary metric for the company’s success, it is no longer the only metric. The Apple story is more diversified than the company gets credit for, and Tuesday night’s earnings report emphatically proves it.

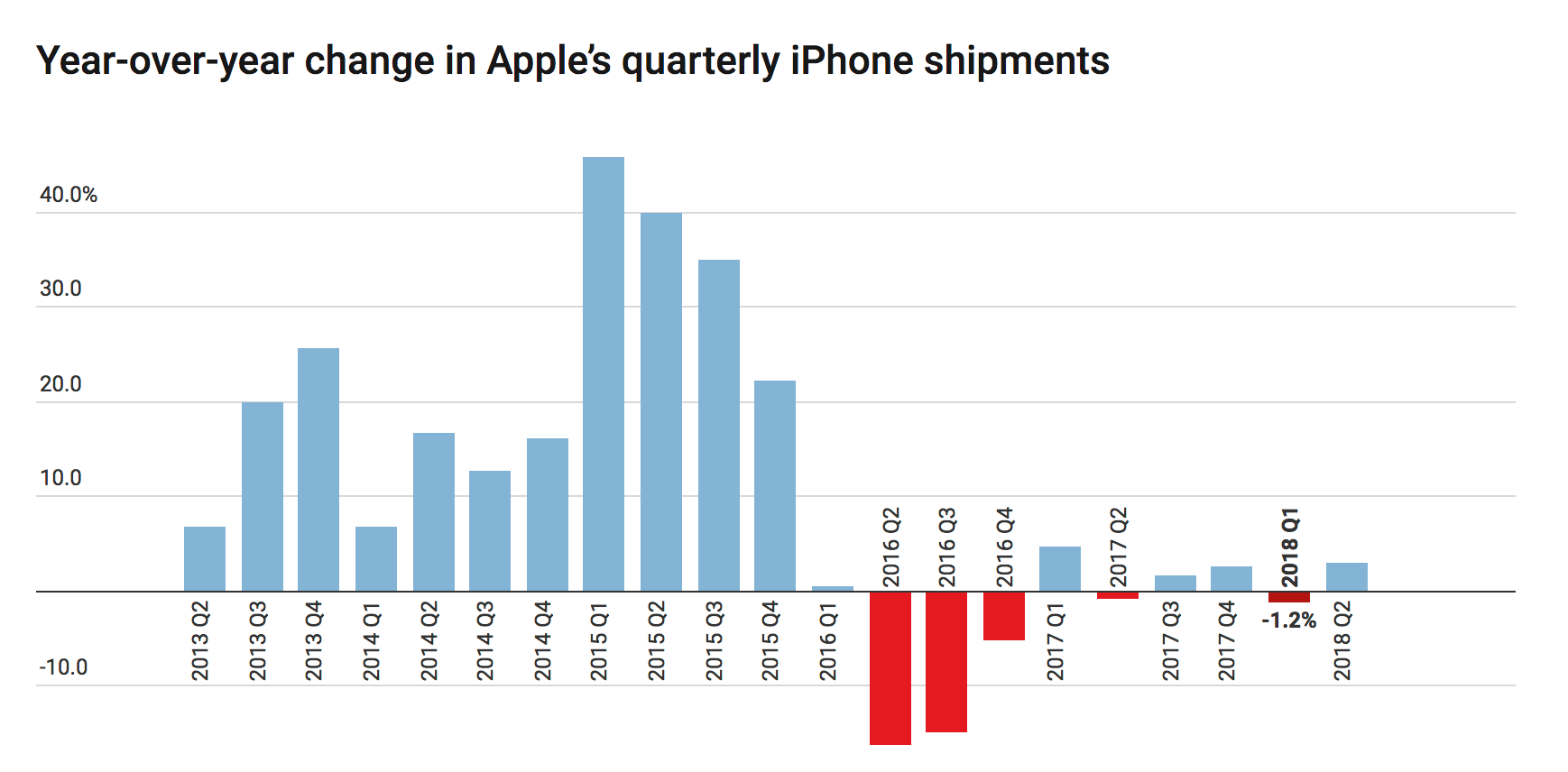

Apple sold 52.5 million iPhones in the first three months of 2018, missing analyst projections of 53 million units sold. That’s a relatively meager 3 percent growth. As you can see in the chart below from Recode’s Dan Frommer, Apple’s unit growth has gone sideways for the past two years.

And yet, Apple’s shares since the start of 2016 are up a whopping 81 percent. The S&P 500 is only up 31 percent over the same period.

Why is Apple on a tear? A few reasons.

First and foremost: The iPhone, even at a low-to-no growth rate, is a killer business. It’s highly profitable, and Apple has managed to raise the average price of the iPhone.

With that cash machine, Apple has gone on a massive stock buyback run, while also raising its dividend. In the first three months of this year, Apple spent $23.5 billion on share repurchases. Since 2012, Apple has spent $200 billion on buying back its shares. It has returned an additional $75 billion to shareholders over that period in the form of dividends. And on Tuesday, it said it would initiate an additional $100 billion in stock repurchases.

No matter what happens with the iPhone, in terms of growth, the fact that Apple has a $300 billion-plus stock buying bazooka helps to soften any blow in the growth of the iPhone for investors.

But beyond that cash bazooka that is sitting on the desk of Apple’s CFO, there’s the fact that Apple has real growth in two new categories.

On the call Tuesday night, Tim Cook said Apple’s “wearables” business was up 50 percent and is now the size of a “Fortune 300” company. That implies its wearables — which include the Apple Watch, AirPods and Beats — is a $9 billion annual business, which is growing at a 50 percent rate. Cook said the Apple Watch grew at a “strong” double-digit rate and had its best ever March quarter performance.

While many analysts and pundits like to focus on where Apple might be missing, they tend to overlook where it’s hitting. And the wearable market between the watch and headphones appears to be dominated by Apple, with no real competition. The closest competitor is Fitbit, a $1.4 billion company whose sales and market value have tanked in the past year.

Apple has the wearable market all to itself right now. And, all signs point toward Apple accelerating its development in the category. There are multiple reports that Apple is exploring the creation of a pair of augmented reality glasses. While Google, and others, have failed with glasses, Apple has a proven track record of selling sexy consumer computing products. Because of the failures by Google and others, there’s a strong possibility that in five years, Apple will be owning the consumer’s face with glasses, the consumer’s wrist with the watch and the consumer’s ears with AirPods.

Meanwhile, the rest of the tech industry is fighting to sell people smart speakers for their kitchen. (Which, by the way, Apple is also doing, so it’s not like it’s totally whiffing on that category!) As they fight over that market, Apple is moving to own wearables.

The final piece of the Apple story is services, which is Apple’s App Store, Apple Music, iCloud and Apple Pay.

Apple says it now has 270 million paid subscriptions, which is up 100 million on a year-over-year basis. Services delivered $9.2 billion in revenue, which was up 30 percent on a year-over-year basis. And, according to Cook, the services growth was global. He says the “minimum” growth for services was 25 percent in each geography.

The services revenue is, for all intents and purposes, and ongoing tax on Apple’s users. If you own an iPhone, you probably subscribe to iCloud to expand storage. If you own an iPhone, you probably download apps and make in-app purchases. If you own an iPhone, you might even be an Apple Music subscriber. Apple doesn’t break out its margin on this business, but it would appear to be a relatively light lift for Apple, so it should be a highly profitable business since, and it should be a business that steady, and growing.

So, in summary: Apple has a potentially great future business in wearables, it has an amazing current business with iPhones, and it has a nice steady recurring revenue business with services. No matter how negative analysts or pundits want to get around the iPhone, the simple fact of the matter is that Apple is well balanced for the future, just as much as any other major tech company.

Source: Tech CNBC

Apple proved that it is no longer just an iPhone company